I think this can only be described as generational theft . . . we’re going to amass the largest debt in the history of this country by any measurement. And we’re going to ask our kids and grandkids to pay for it.

Sen. John McCain

Face the Nation

Feb. 8, 2009

Amid all the conservative caterwaling about the stimulus package and the mortgage relief program and TARP II and the varous other elements of Obama's fiendishly clever plot to enslave future American generations by burdening them with mind-boggling levels of debt, I thought it might be informative to look at where the country stands, debt-wise, and how we got here.

Hint: It isn't Uncle Sam's fault.

Debt definitely has exploded -- and now equals roughly 350% of US GDP, which, according to George Soros(who should know) is more than twice the debt burden shouldered by the American economy on the eve of the 1929 crash and the Great Depression. And thanks for pointing that out, George.

The trend towards ever greater debt ratios has been particularly steep since then mid-1990s, which was roughly when the global creditor class decided that the "Great Moderation" (the globalization-induced taming of both inflation and recession) was here to stay, and began shoving loans in the face of any borrower who could fog up a mirror -- and some who couldn't.

There is an on-going economic debate -- too wonkish and tedious to explore here -- about whether this wall of money was a result of a coincident collapse in personal saving in the US, the UK and some of the other wealthy countries, or whether it actually caused middle-class and upper-middle class consumers to go an a spending spree the likes of which the hasn't been seen since the invention of the credit card.

Suffice it to say both sides of the trade thought they were getting a great deal at the time. And many of the same right-wing financial pundits now bitching about all this debt were perfectly happy to invent sunny stories that explained why it could go on forever:

"The structure of the household portfolio has changed over time," said David Malpass, chief economist at Bear Stearns.

Life is full of little ironies like that.

Of course, conservative gospel tells us private debt is never a problem -- even when it's used to turn houses into ATM machines. But government borrowing (the only type of IOU dignified with the label "national debt") is always a problem, even when it's used to build roads and bridges for all the cars bought with all that equity extracted from all those overpriced suburban mini-mansions. Then it's "porkulus".

However, note the green line at the bottom of the chart. Despite the best efforts of Ronald Reagan, George I and George II, government debt (federal, state and local) relative to the size of the US economy is only a hairline higher than when Gerald Ford was in the White House. At about 50%, it's well below most of the other major wealthy countries, including Japan (180%), Italy (120%), France (70%) and even those debt-phobic Germans (60%).

So how did total US debt (the real "national" debt) get so high? Well, in addition to the debt-financed consumption boom, we saw an even bigger (as in Hiroshima-sized) explosion in financial debt -- which is to say, borrowings between banks and other financial institutions.

Much, although not all, of this debt was used to finance leveraged investments in various paper assets, thus pumping up their prices, thus making it easier borrow and invest in real assets (homes, office buildings, companies), thus pumping up their prices, thus creating the wonderful bubble we all enjoyed so much. And, not incidently, creating quasi-gainful employment for hordes of commodity traders (boring stuff like grain, metal and pork bellies having long since given way to financial futures as the life's blood of the Chicago Mercantile Exchange), thus enabing financial "journalists" like Rick Santelli to be paid ridiculous sums of money to throw childish temper tantrums on TV.

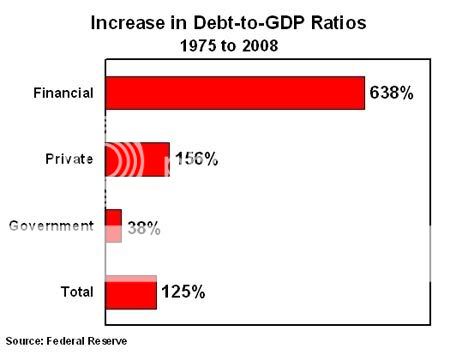

The chart above doesn't really do this orgy of paper spinning full justice, since it started from a very low base -- an earlier generation of bankers and brokers having had some lingering ancestral memories of what happens to over-leveraged financial institutions (or even normally leveraged ones) in a rip-roaring deflationary spiral. So I whipped up this chart:

A six-fold increase in the financial debt-to-GDP ratio, versus a piddling 38% increase in government debt to GDP -- over a 33-year period. That works out to an 8% rate of growth in government debt, versus a 7% rate of GDP growth (including inflation) and almost a 14% rate of growth in financial debt.

Since the early '90s those numbers have gotten even more lopsided, thanks to Washington's brief fling with fiscal discipline: 4% growth in government debt, which was less than the 5.3% rate of GDP growth. Financial debt, however, continued speeding along at double-digit growth rates -- that is, until last September, when it plowed into a brick wall.

Conventional wisdom used to hold that financial debt really didn't matter much because the banks "owed it to themselves." This meant that if you netted out all their obligations to each other, they summed to something approximating zero. This, funny enough, was exactly the same argument used by the financial industry to justify allowing an unregulated derivatives market to grow to something like $70 trillion in "notional" contract value.

What we've since learned, much to our sorrow (particularly those of us who are, or at least were, Citigroup shareholders) is that saying the banks "owe it to themselves" isn't much help if they all decide simultaneously they want themselves to pay themselves back. Because the unwinding of all that leverage, while it might not directly bankrupt the banks (although some will fare worse than others in the process) has a direct, immediate and powerful effect on asset values -- which most definitely can bankrupt them and us, too.

This is the process that an economist of the Great Depression era, Irving Fisher, labeled "debt deflation": As banks shrink their balance sheets, money and credit contracts. As money and credit contracts, prices (first of assets, then of commodities, labor and everything else) start to fall. Falling prices (deflation) increase the real value of outstanding debts while at the same time reducing the cash flows needed to service those debts. This forces more borrowers to default, forcing banks to shrink their balance sheets even more, causing prices to fall farther and faster. Rinse and repeat, until the banks (and the economy) are laying flat on their backs, with little tags attached to their big toes.

We've been down that spiral once before, and the results were sufficiently terrible to leave the next two generations of Americans with a morbid fear that it might happen again.

But now -- even as the Great Depression has faded almost from living memory (allowing a new generation of conservative ideologues to lie with impunity about its causes and cures) -- there is a very definite risk that it will happen again.

Last year, the growth of private debt abruptly slowed and has probably (we only have data through the 3rd quarter) turned negative. The consequences can be seen at the tail ends of the lines in the first chart: Even as GDP has contracted, the financial debt-to-GDP ratio has flattened, while the private debt-to-GDP ratio has actually turned down. Debt is now contracting faster than GDP.

History suggests that, left to its own devices, this trend will not last -- but only in the sense that things will get even worse. That is, if deflation really does get a firm grip on the economy, GDP is likely to implode faster than debt can be paid down or written off, causing debt ratios to start rising again.

The ever helpful Soros points out that debt went from 160% of GDP at the time of the 1929 crash to 260% by 1932, overwhelming both the natural forces (pent-up demand, cheap wages, the tendency of price deflation to increase the real money supply) that might otherwise have helped the economy find a bottom, as well as the Hoover Administration's feeble efforts to stimulate demand.

Why hasn't this happened again (yet)? Because the Federal Reserve has partially offset the contraction in private financial debt by adding more than $1 trillion to its own balance sheet over the past year. Because the TARP program, as corrupt and wasteful as it's been, at least has prevented an even bigger, nastier contraction in private credit. And because the US Treasury has stepped up its own borrowing to pay for TARP and to cover the higher spending and falling revenues brought about by the recession.

In other words, because of all the things that seem to be driving CNBC reporters and other assorted wingnuts completely insane.

To my mind, this is a variation on the old saying that if you don't know where your food comes from or your shit goes, you're in big trouble. The hard truth is that there is now only one, and only one entity on the planet that can keep the private credit excesses of the past decade, which most conservatives wildly applauded, from ending in a classic debt-deflation meltdown. And that is the US federal government.

This being the case, we're lucky federal debt is as low as it is. Former IMF economist Simon Johnson has estimated that the necessary fiscal stimulus, plus the tab for cleaning up the banks, will take federal debt in private hands (as oppposed to the total debt shown in the charts above, which includes the Social Security trust fund) to something north of 70% of GDP, from the current 41%, by the time the crisis is over.

Update 2/22: The parenthetical text above is just plain wrong: The Fed nets out the Social Security trust fund in the flow of funds accounts. That being the case, I'm not sure why Simon Johnson's federal debt-to-GDP ratio is lower than the mine, unless he is also netting out some of the other federal trust funds that hold Treasury debt, like the civil service retirement fund. The Fed seems to thinks those debts should be treated as "real" liabilities, instead of an inter-agency bookkeeping entry, like the Social Security trust fund. I frankly don't understand the logic behind this distinction, so maybe Johnson is right, in which case the federal debt burden is actually lower than what's shown on my chart.

On the other hand, you could also argue that all Treasury securities (whether held by government trust funds or by private investors) should be treated as "real" debt, in which case the federal debt burden is higher, more in the range of 70-80% of GDP.

Sorry to go all wonkish about this, but some commenters were quarreling with my numbers, and I wanted to make sure I've got it straight.

That's a major hit to Uncle Sam's creditworthiness, and it's going to create major financing problems for him -- even if he is the owner and sole proprietor of the world's dominant reserve currency. But, if there's one thing I've consistently underestimated over the past two decades, it's the appetite of global creditors for dollar assets. The day may yet come when that particular stomach bursts. For now, though, all the incentives are for our creditors to keep Uncle Sam afloat. In a world sliding rapidly towards deflation, the alternative, for them as well as us, would be the economic equivalent of a murder-suicide pact.

A bigger worry is the gearing. Private debt has gone from less than three times government debt in 1975 to more than five times today. So even if private debt only flattens out, instead of contracting, it could take a fairly heroic rise in federal debt to break the downward spiral in employment, prices and production. Do Obama and the Democrats have the political will, and the votes, to do what's necessary? The latest signs are not good.

President Obama will seek to cut the federal deficit in half by the end of his first term, according to an administration official.

Hopefully, this was just the modern version of St. Augustine's famous prayer ("Lord, help me be good, but not just yet"), publicly uttered in an attempt to reassure the world's lenders that Uncle Sam is still a reasonable credit risk. You may recall the previous president also promised to cut the deficit in half by the end of his second term, without ever taking any concrete steps to do so.

But even if the Obamanauts don't really mean it, the years of anti-government and anti-deficit propaganda have definitely left their mark -- not least on the village idiots of the Beltway media, who may not rant and rave on camera, but who can't even comprehend, much less accept, the idea that there are times when expanding government debt is not only not a bad thing, but is a positive good thing, even an essential thing. The Keynesian idea of fighting a recession brought on by excessive debt with more debt is a hopelessly counterintuitive strategy. And intuition, for better or worse, is what democracy runs on most of the time -- that is, when it isn't being powered by base emotions like greed, fear and hatred.

Maybe there is no way out of this mess, either practically or politically. Limitless growth, Edward Abbey once wrote, is the ideology of a cancer cell, and the doctrine of endless debt-fueled expansion may have created an economy so riddled with it that any therapy powerful enough to kill the cancer will also kill the patient. In other words, globalized capitalism (or rather, this strange brew of corporate oligopoly and lemon socialism) may have finally dug itself a hole too deep for the traditional neo-Keynesian policy tools (fiscal and monetary policy) to lift it out of.

But, if that's true, then our children and our grandchildren may indeed spit on our graves, but it's going to be because we have bequeathed them much bigger nightmares than an increase in the federal debt.